Understanding German Tax Classes: Why Employees on the Same Salary Don’t Always Take Home the Same Pay

Understanding German Tax Classes: Why Employees on the Same Salary Don’t Always Take Home the Same Pay

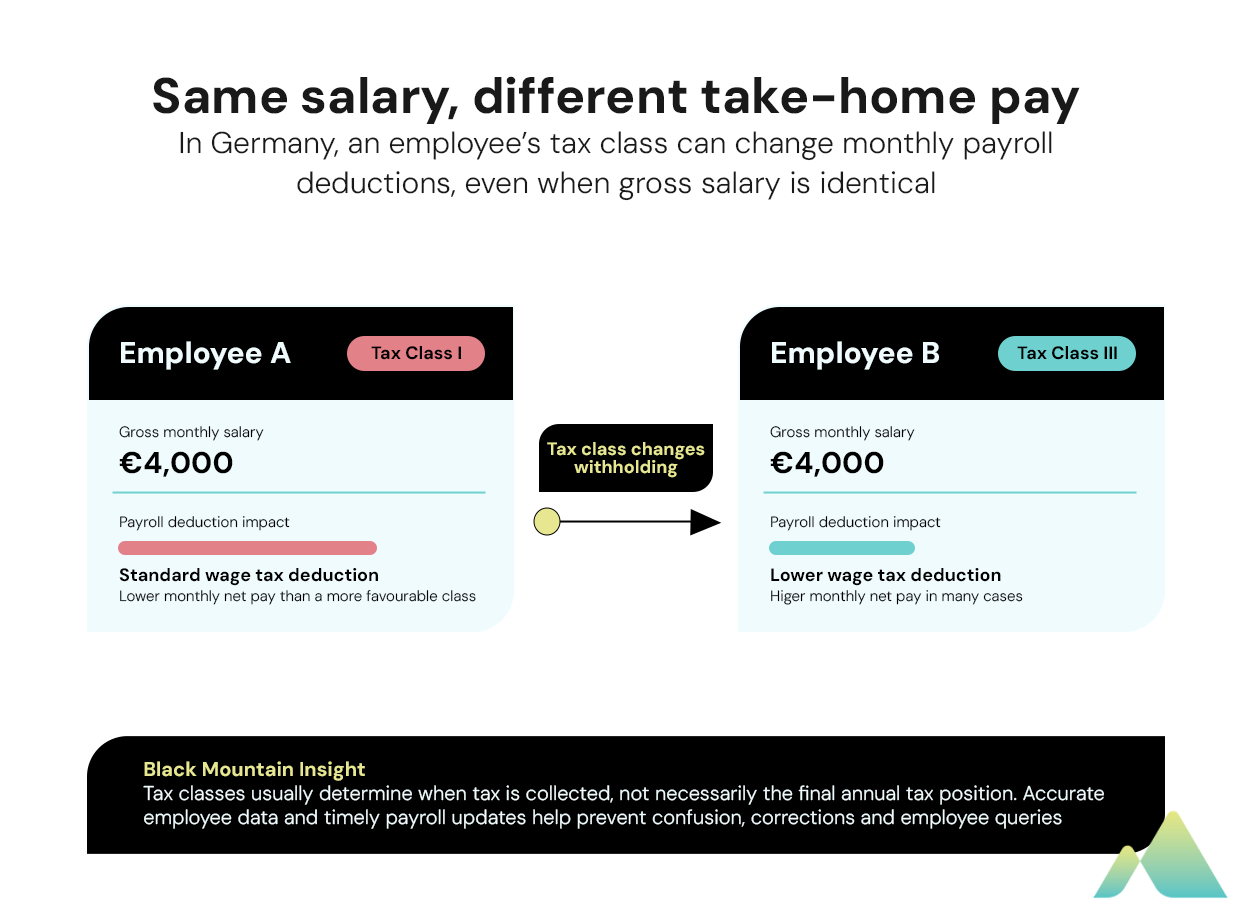

Imagine two employees in Germany earning exactly the same salary.

They work for the same employer, perform similar roles and receive the same annual pay increase. Yet when payday arrives, one employee takes home significantly more than the other.

For employers unfamiliar with the German payroll system, this can seem confusing. For employees, it can lead to questions, concerns and sometimes the assumption that a payroll error has occurred.

In reality, the difference often comes down to one thing: German tax classes (Steuerklassen).

Understanding how tax classes work is an essential role for anyone managing payroll in Germany. While German tax classes do not ultimately determine how much tax an employee pays over a full year, they can have a significant impact on monthly take-home pay and play an important role in ensuring payroll is processed accurately.

Why Germany Uses Tax Classes

Unlike many countries where income tax is calculated using a relatively straightforward set of rates and allowances, Germany uses six tax classes to determine how much wage tax (Lohnsteuer) is withheld from an employee’s salary each month.

An employee’s tax class is generally based on factors such as:

- Marital status

- Whether they are a single parent

- Whether they have multiple jobs

- Their spouse’s employment situation

The purpose is to ensure that monthly tax deductions more accurately reflect an individual’s circumstances throughout the year.

This means two employees earning the same salary can see very different amounts arrive in their bank accounts each month.

The Six German Tax Classes Explained

Tax Class I

The standard german tax class for:

- Single employees

- Divorced employees

- Widowed employees (after the relevant transition period)

Most international employees relocating to Germany will initially fall into this category.

Tax Class II

Designed for single parents.

Employees in this category benefit from additional tax relief, resulting in lower monthly tax deductions than employees in Tax Class I.

Tax Class III

Typically used by the higher-earning spouse in a married couple where the other spouse is assigned Tax Class V.

This class often results in significantly lower monthly tax deductions and therefore higher take-home pay.

Tax Class IV

Commonly used when both spouses earn similar salaries.

It generally produces more balanced monthly deductions across both employees.

Tax Class V

Often paired with Tax Class III.

Employees in this class usually experience significantly higher payroll deductions than their spouse in Tax Class III.

Tax Class VI

Applied to secondary employment.

This class generally results in the highest level of payroll deductions because standard tax allowances are not applied.

Why Two Employees Can Receive Different Net Pay

This is where international employers often become confused.

A German employee earning €4,000 per month in Tax Class III may take home considerably more each month than another employee earning the same salary in Tax Class V.

From an employer’s perspective, nothing has gone wrong.

The payroll calculation is simply reflecting the tax class recorded by the German tax authorities.

One of the most common misconceptions is that a more favourable tax class permanently reduces tax liability. In reality, tax classes largely determine when tax is collected, not necessarily how much tax is ultimately owed.

The final position is usually adjusted through the employee’s annual tax return.

Why Payroll Accuracy Matters

German tax classes may sound straightforward on paper, but they add another layer of complexity to payroll processing.

A payroll team must ensure employee information is correctly maintained, tax data is updated promptly and calculations reflect any changes communicated through the relevant authorities.

Small administrative mistakes can quickly become larger problems.

According to payroll industry research featured within Black Mountain’s global payroll insights:

- The average cost of a payroll error is approximately $291 per error.

- 49% of employees begin job searching after repeated payroll issues.

While these figures are not specific to Germany, they highlight an important reality: payroll is one of the most visible processes within any organisation. Employees may never see your internal systems, but they notice immediately when their pay is incorrect.

Black Mountain Insight: Tax Classes Are Often Not the Real Problem

When organisations encounter payroll issues in Germany, tax classes are rarely the root cause, the challenge is normally a wider process issue.

We frequently see organisations struggling with:

- Employee onboarding data not being captured correctly

- Delays in receiving tax information

- Disconnected HR and payroll systems

- Manual payroll processes

- Inconsistent record management across countries

Germany’s payroll is highly regulated, with payroll calculations closely linked to tax reporting and social security obligations. As a result, a small data issue can have wider consequences if it is not identified quickly.

For international businesses managing employees across multiple countries, ensuring payroll, HR and finance teams remain aligned is often just as important as understanding the tax rules themselves.

Getting German Payroll Right

Understanding tax classes is an important first step, but accurate payroll in Germany requires much more than applying the correct tax code.

Employers must also manage:

- Income tax withholding

- Social security contributions

- Employee registrations

- Statutory reporting requirements

- GDPR-compliant employee data management

As Germany continues to attract international businesses and talent, payroll remains one of the most critical areas where compliance, employee experience and operational efficiency intersect.

Tax classes are just one piece of the puzzle, but understanding how they affect take-home pay can help employers answer employee questions with confidence and avoid unnecessary payroll complications.